Latest Dispatch

Security Starts at Home: A Timely Reminder for Every Australian

A police reminder issued this week may have been aimed at Coober Pedy residents, but the message is one that applies to communities across Australia. With opportunistic property crime continuing to affect towns and ci...

Read the full story →More From The Telegraph

Community, Culture and Connection Celebrated at Coober Pedy's Serbian Orthodox Parish Slava

Coober Pedy's rich multicultural heritage was on full display on Sunday as the Serbian Orthodox Church of St Prophet Elijah welcomed visitors from across Aus...

Human remains discovered in Andamooka mine shaft as police investigate

South Australia Police have launched an investigation after suspected human remains were discovered inside a mine shaft at Andamooka, raising fresh questions...

Crime Should Be Reported. Fear Shouldn't Be Manufactured.

There is no question that Coober Pedy has experienced a handful of concerning incidents in recent weeks. Overnight vehicle thefts, break-ins and property cri...

Opinion: If Your Business Needs to Push Others Down, Is It Really a Business Worth Supporting?

# Opinion: If Your Business Needs to Push Others Down, Is It Really a Business Worth Supporting? There is an old saying that a rising tide lifts all boats. I...

Opinion: Anger Is Understandable, But It Needs Direction

The past week has tested Coober Pedy. Vehicle thefts, break-ins and other criminal activity have understandably left many people frustrated, angry and, in so...

Overnight Crime Spree Rocks Coober Pedy

Residents are being urged to check their security cameras and dash cams after a series of thefts and break-ins across Coober Pedy overnight. Police are inves...

What happens when the taps—and the revenue—are turned over?

For decades, the District Council of Coober Pedy has been unlike almost every other council in South Australia. Not only has it run the town, it has also ope...

Opinion: If the decision was already made, why ask the community?

When the District Council asked residents to suggest a name for the new road through the Black Flag opal field, many saw it as an opportunity to recognise th...

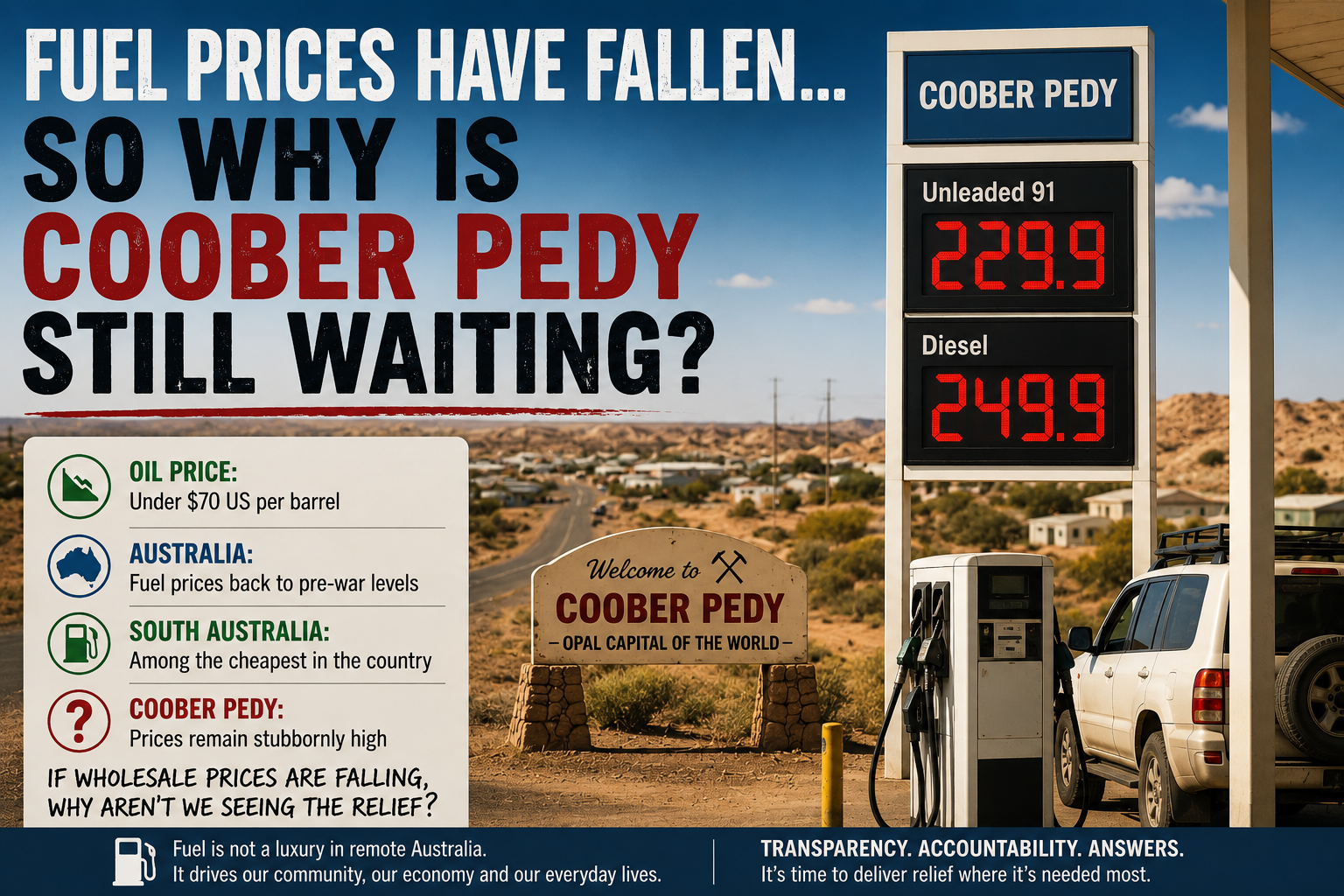

Fuel Prices Have Fallen… So Why Is Coober Pedy Still Waiting?

Australian motorists are finally receiving some long-awaited relief at the bowser. After months of volatility caused by conflict in the Middle East, fuel pri...

Elderly Coober Pedy Man Dies Following Mobility Scooter Crash

Elderly Coober Pedy Man Dies Following Mobility Scooter Crash An 84-year-old Coober Pedy man has died following a road crash involving a mobility scooter and...

Festival Preparations Interrupted by Unexpected Kangaroo Encounter

As volunteers across Coober Pedy busily prepared for the opening of this year's Opal Festival, one local family found themselves dealing with a very differen...

Archie Road: A Name Worthy of Coober Pedy's History

Coober Pedy residents are currently being invited to provide feedback on the naming of a new road. The options put forward include names such as Magazine Roa...

Serious crash: Bulgunnia

Police and emergency services attended the scene of a serious crash at Bulgunnia in the Far North early Tuesday morning following a collision between a road ...

Government announce $7.2 million campaign for diphtheria vaccination

As health authorities intensify their response to Australia’s growing diphtheria outbreak, many residents across remote communities are beginning to ask diff...

Coober Pedy Policing Debate Raises Bigger Questions for the Town

A recent industrial dispute involving staffing levels at the Coober Pedy police station has once again placed the town under an uncomfortable spotlight, with...

Opinion Piece: Why Now? Coober Pedy Faces Uncertain Future Under Native Title Shift

Coober Pedy has always been a town built on grit, independence, and a unique relationship with the land. For over a century, opal miners, pastoralists, and l...

Coober Pedy: Governed to the Brink

Coober Pedy has now spent years under administration. Not led by locals. Not guided by elected representatives. But run by government-appointed administrator...

We Called It – And Now the Evidence Is Piling Up

When we first raised serious concerns about the integrity of the recent South Australian election, we were dismissed by some as being too harsh, too early, o...

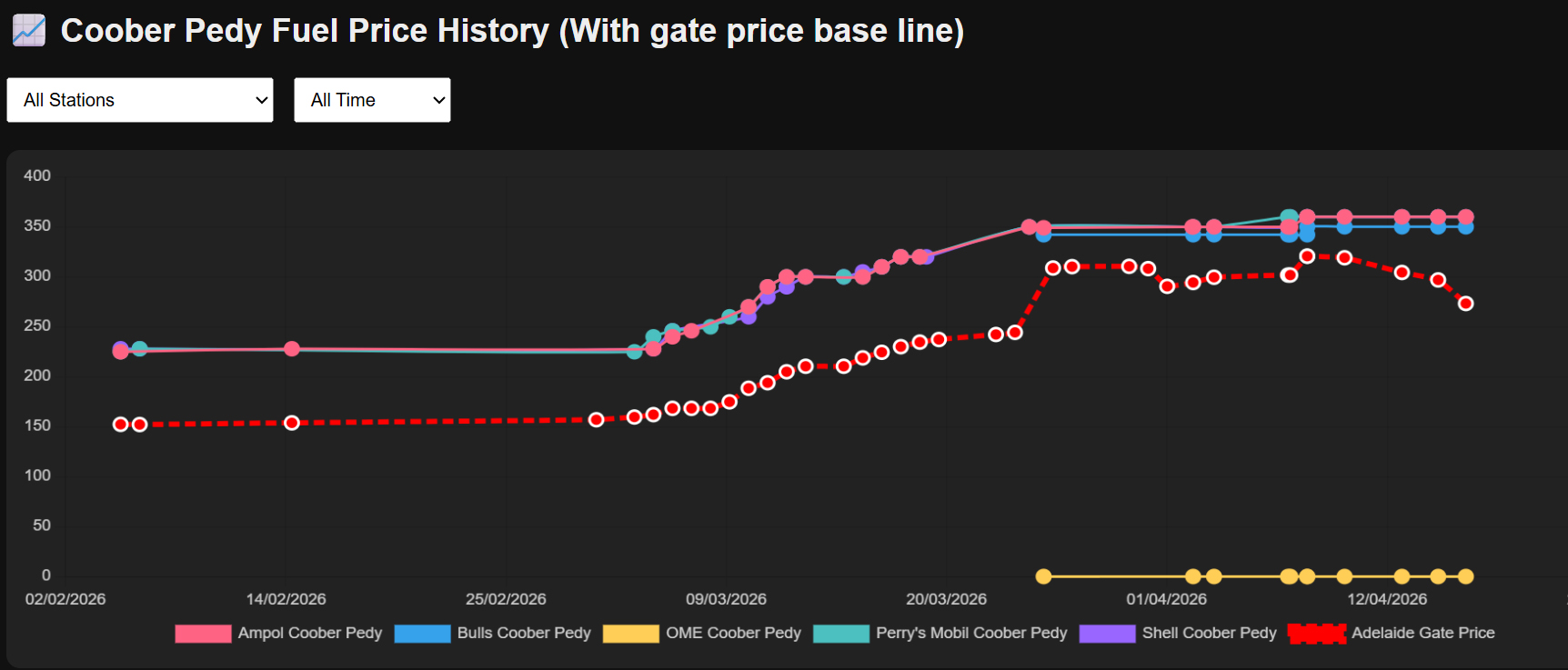

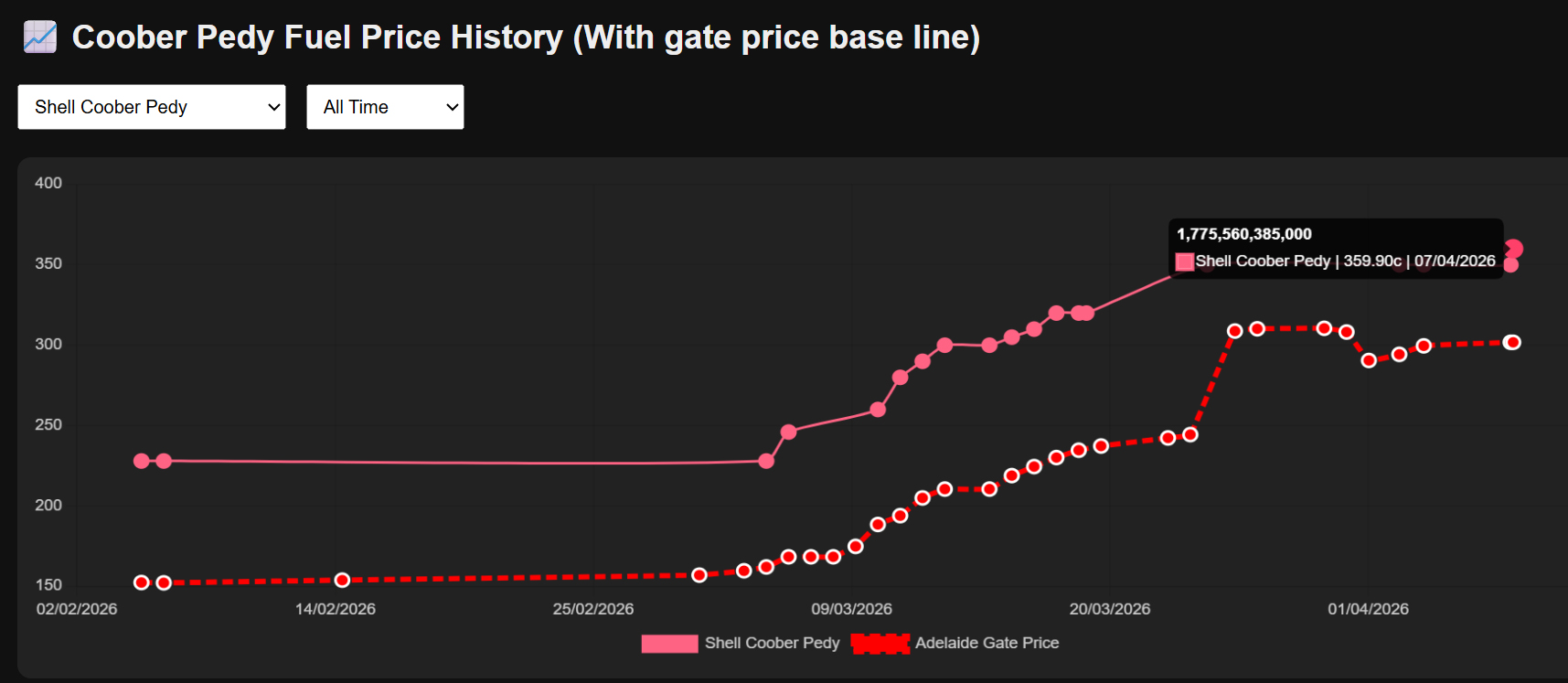

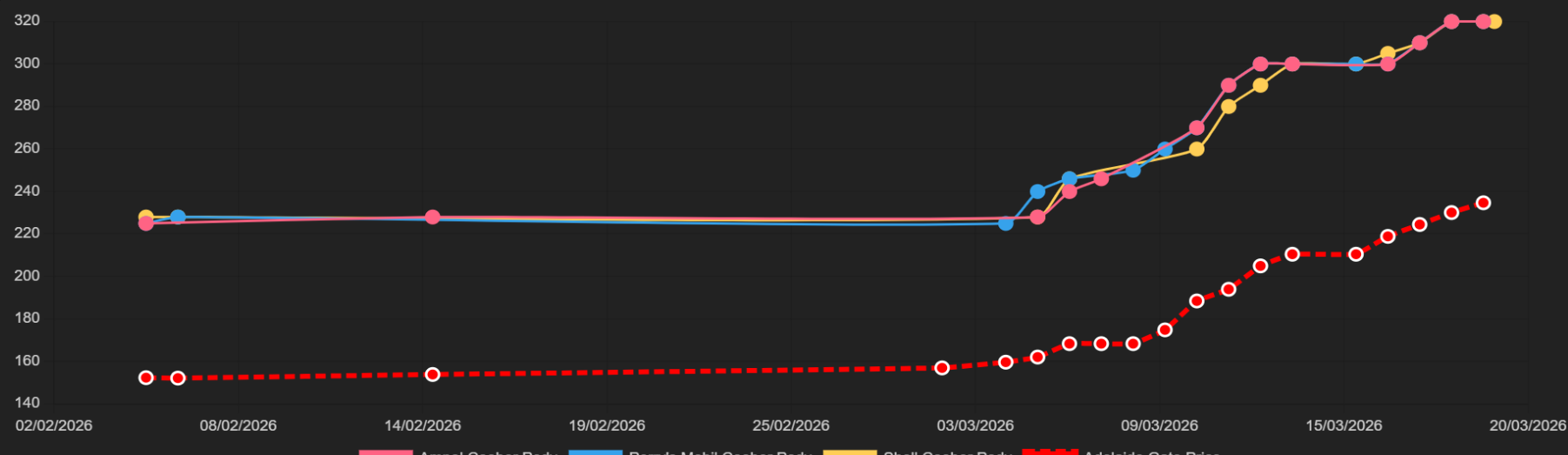

Coober Pedy Misses Out as Fuel Prices Refuse to Budge Despite 26c Relief

Motorists in Coober Pedy are being left scratching their heads—and digging deeper into their pockets—after fuel prices in town have failed to move, despite c...

Fuel Excise Cut Fails to Deliver as Prices Surge Again in Coober Pedy

The Federal Government’s decision to halve the fuel excise was meant to provide immediate relief at the bowser. From 1 April 2026, the excise on petrol and d...

Historic First: Opalised Octopus Discovered in Coober Pedy

A remarkable discovery in Coober Pedy’s famed opal fields has sent shockwaves through both the mining and scientific communities, with what is being describe...

Price of Australia’s National Gemstone Tipped to Rise Sharply as Fuel Costs Bite

The global fuel crisis is beginning to ripple far beyond the bowser, with early signs emerging that the price of Australia’s national gemstone—opal—could be ...

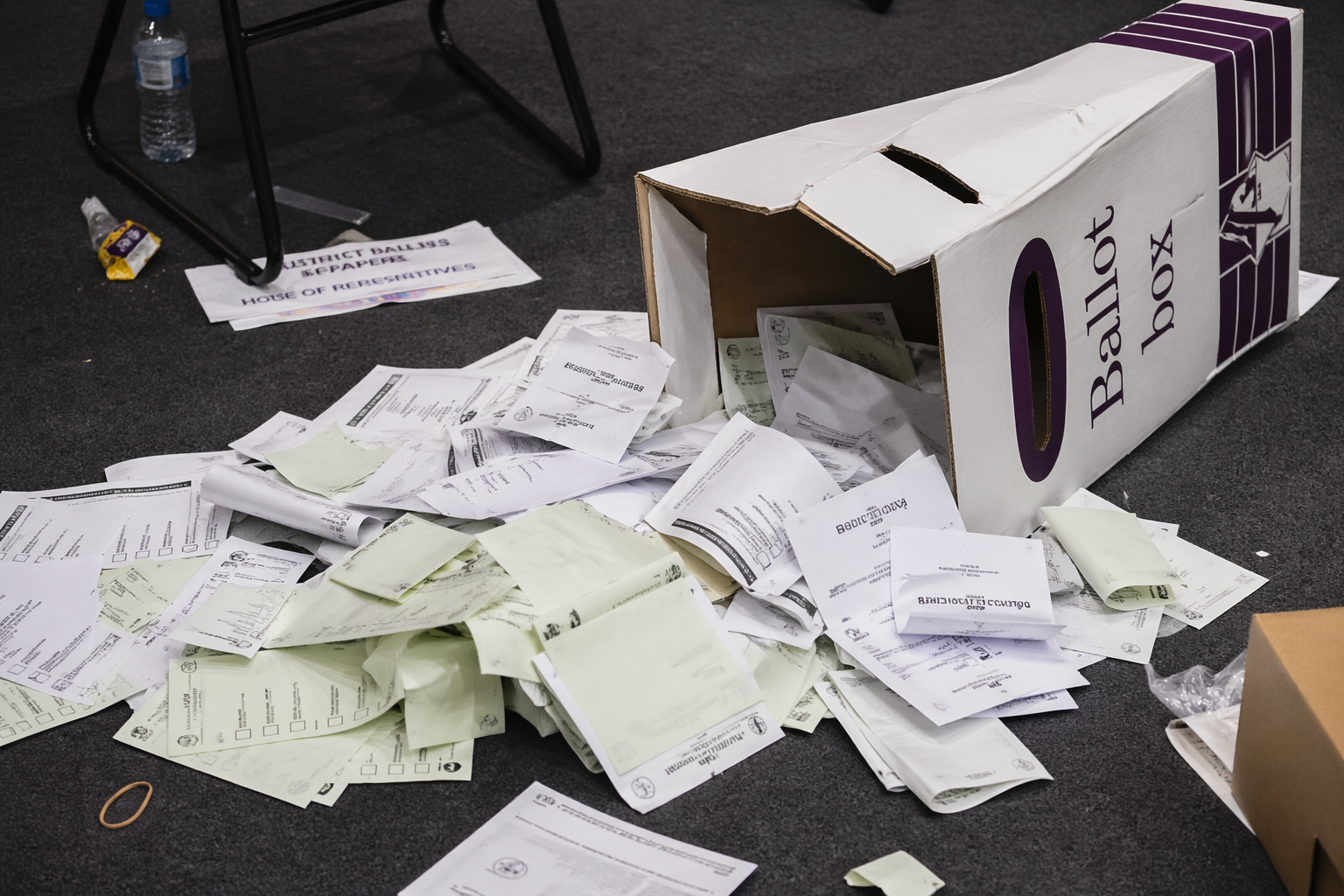

Hundreds Still Silenced: New Figures Confirm Scale of Coober Pedy Voting Failure

New figures released today by the ABC News have confirmed what many in Coober Pedy already knew — a significant portion of the town was shut out of the democ...

Coober Pedy Fights Back — But Questions for ECSA Are Only Just Beginning

The Electoral Commission of South Australia (ECSA) may believe the matter is settled. For the people of Coober Pedy, it is anything but. After what can only ...

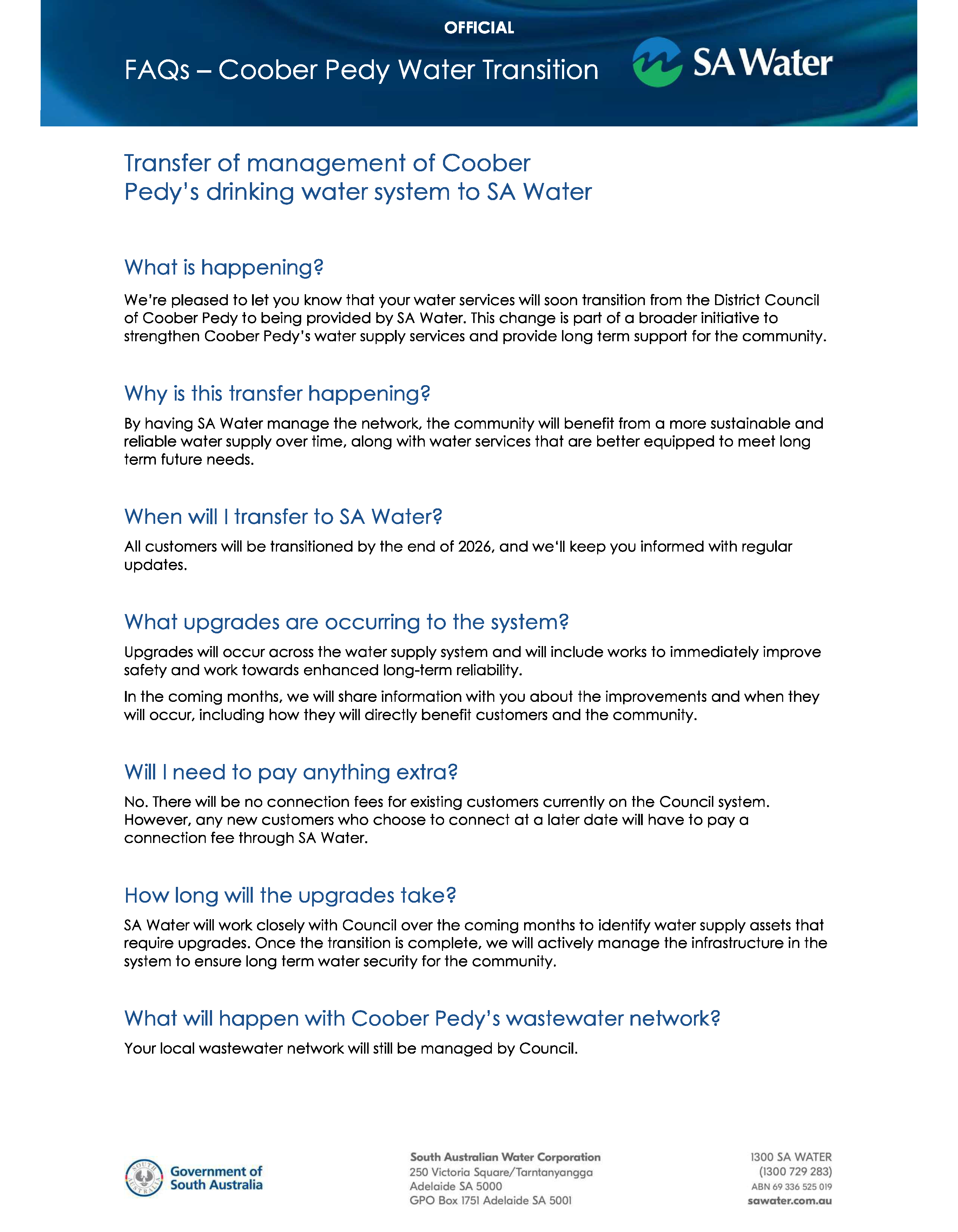

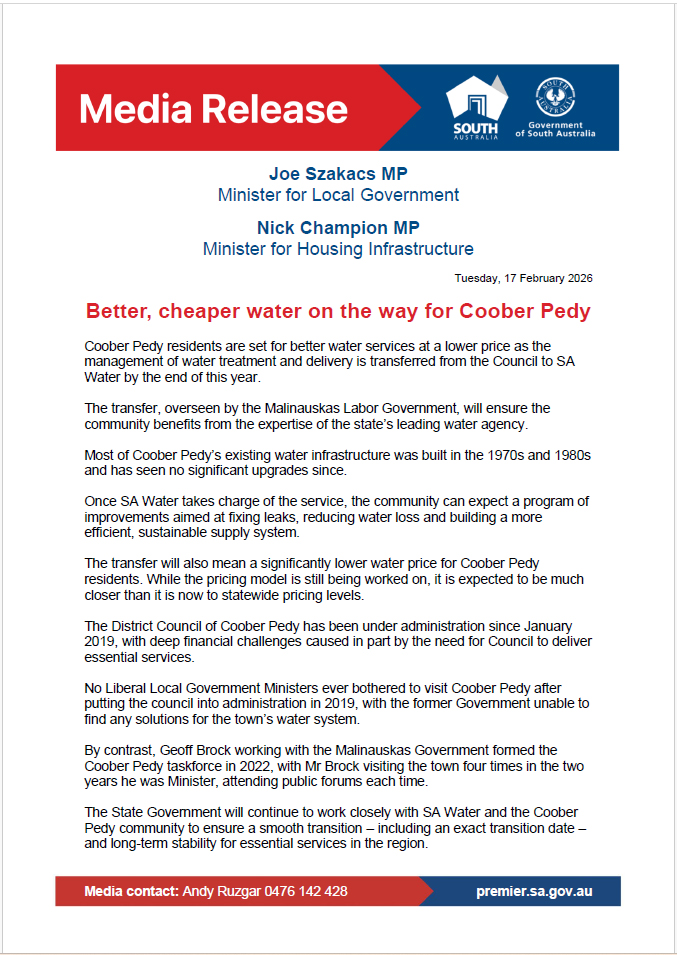

Coober Pedy Water Transition Confirmed, Marking Long-Awaited Shift for Town

The transition of Coober Pedy’s drinking water system to SA Water has been formally confirmed, bringing an end to years of discussion and uncertainty around ...

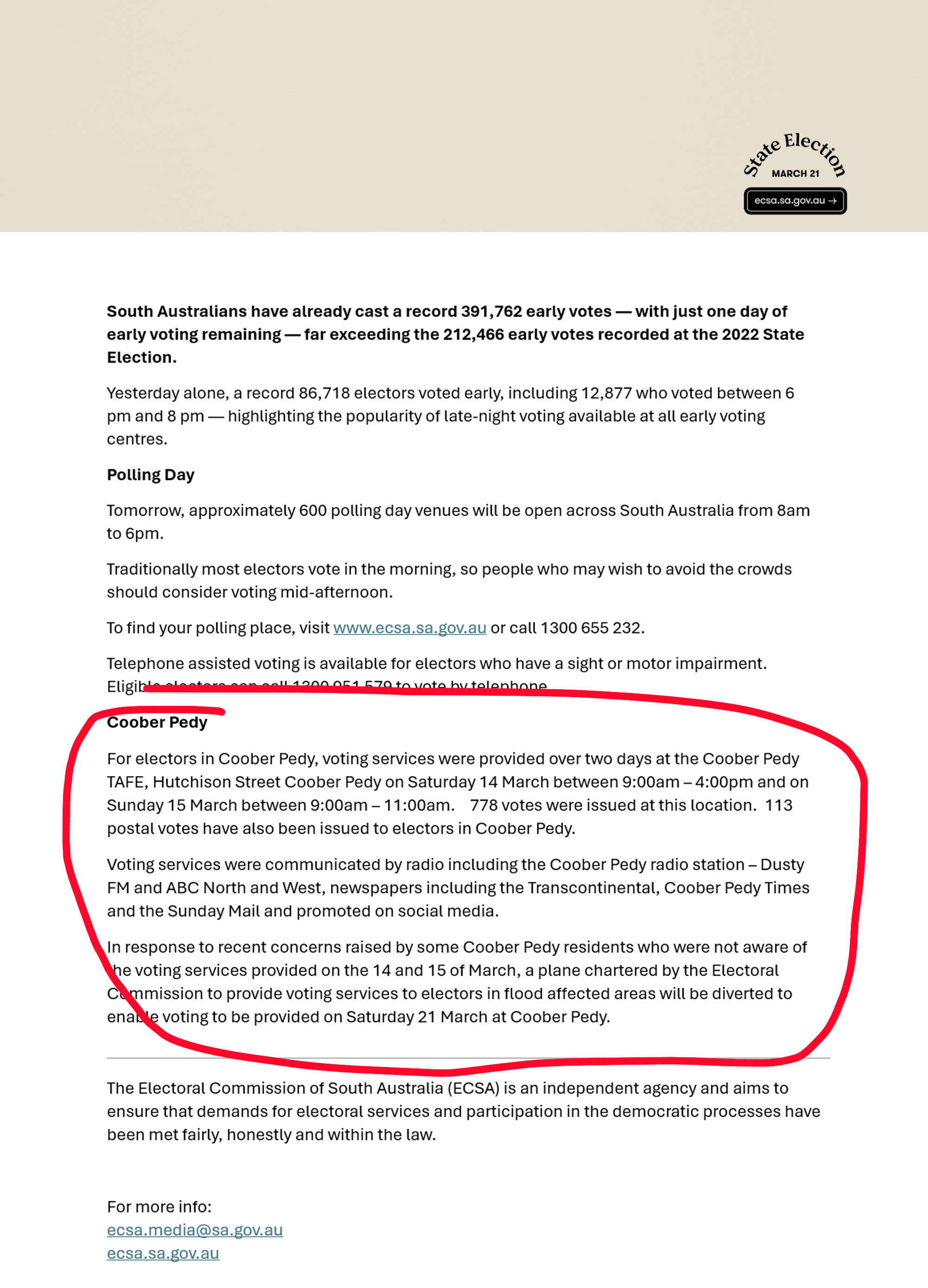

URGENT: Voting Returning to Coober Pedy Tomorrow — But Key Details Still Missing

Residents of Coober Pedy are being urged to stay alert after new information emerged today confirming that voting will take place in the town tomorrow (Satur...

Outback Fuel Prices Under the Microscope: Coober Pedy Paying a Heavy Price

Residents of Coober Pedy have long accepted that living in one of Australia’s most remote towns comes with higher costs. Freight, logistics, and isolation al...

Voting Confusion Sparks Anger in Coober Pedy

Confusion over altered polling dates in Coober Pedy has sparked anger among residents, with many claiming they were unaware that voting in the town effective...

Remote Communities Told to Vote Tomorrow – But No One Was Told

Residents of Coober Pedy and other remote South Australian communities have been left stunned tonight after discovering that their opportunity to vote in the...

37th Coober Pedy Opal Festival Announced

Preparations are now officially underway for the 37th Coober Pedy Opal Festival, with organisers today announcing the return of the town’s biggest annual com...

Fuel Prices Surge in Coober Pedy as Global Conflict Raises Familiar Questions

Residents and travellers in Coober Pedy are once again facing eye-watering fuel prices, with diesel now pushing $2.79 per litre in town. The latest spike has...

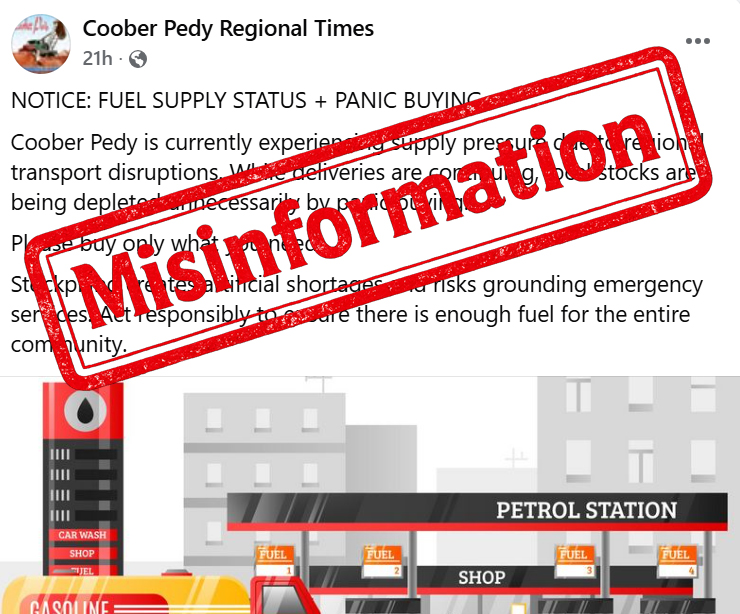

Fuel Fears in Coober Pedy Unfounded as Social Media Claims Spark Unnecessary Concern

Social media claims suggesting fuel shortages and rationing in Coober Pedy appear to be unfounded, despite recent posts circulating online warning of panic b...

Two Minute Noodlers Brings Fresh Energy to Coober Pedy

A new business is set to bring a burst of creativity and much-needed services to Coober Pedy, with “Two Minute Noodlers” opening on the corner of Hutchison S...

Lunar Eclipse Draws Eyes to the Skies Over Coober Pedy

Locals across Coober Pedy stepped outside last night to witness a spectacular lunar eclipse, with many treated to the striking sight of a deep red “Blood Moo...

Fringe in the Desert… Again. But Who Is Driving It?

Last year Coober Pedy was told that bringing Adelaide Fringe to town was a bold cultural step forward. We were assured it was a success. When questions were ...

Shell Coober Pedy Recognised in National Company Awards

Shell Coober Pedy has been recognised with three honours in Shell’s internal “People Make the Difference Real” awards program. The awards, run nationally by ...

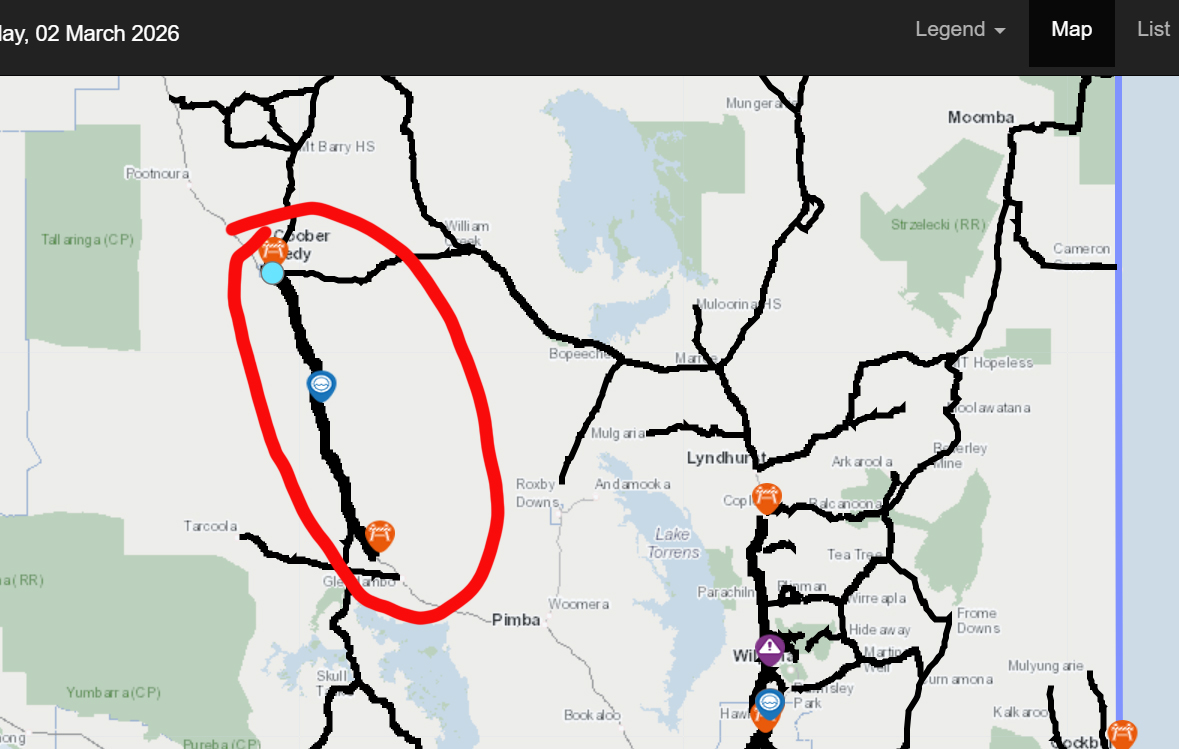

Stuart Highway Closed Between Glendambo and Coober Pedy After Significant Road Damage

The Stuart Highway has been closed between Glendambo and Coober Pedy following significant road damage near the Buzzard area, adjacent to the Peak Mines oper...

Coober Pedy Showcases Outback Spirit at SA Caravan & Camping Expo

Coober Pedy is proudly flying the flag for outback South Australia this week at the South Australia’s Caravan, Camping & Outdoor Show, one of the state’s lar...

Coober Pedy Showcases Outback Spirit at SA Caravan & Camping Expo

Coober Pedy is proudly flying the flag for outback South Australia this week at the South Australia’s Caravan, Camping & Outdoor Show, one of the state’s lar...

HomePolice newsSA Police NewsTrafficDrink driver towing a car in Coober Pedy Drink driver towing a car in Coober Pedy

A drink driver was detected by police at Coober Pedy last night while he was towing another car. Police pulled over a ute on Flinders Street, Coober Pedy jus...

SA Water to Take Over Coober Pedy Supply — Long Overdue Reform or Election-Eve Promise?

Coober Pedy residents have been promised something they have been asking for, loudly and consistently, for many years: the transfer of the town’s water manag...

Brandon Turton Visits Coober Pedy, Hears Concerns from the Ground

Coober Pedy, SA — One Nation’s candidate for the vast electorate of Stuart, Brandon Turton, spent the weekend in Coober Pedy, meeting with locals, touring th...

Coober Pedy: Paying the Most, Getting the Least

There is something deeply wrong in Coober Pedy. For years, our 1-kilometre dirt road — a main access route used by tourists, freight operators and livestock ...

Citizen of the Year Award Finally Reflects the Community

Each year on Australia Day, South Australia recognises individuals whose quiet, tireless service strengthens the social and cultural fabric of their communit...

Opinion: Coober Pedy Has Been Warning You for Years – Now the System Is Breaking

For those of us who live in Coober Pedy, none of this comes as a surprise. The latest revelations about dangerous police shortages, community constables bein...

Driver escapes serious injury

A driver has narrowly avoided serious injury after crashing into a licensed premises in Coober Pedy overnight. Police were called to Hutchison Street about 1...

Teen to Face Youth Court Over Coober Pedy Break-In and Car Theft

A 17-year-old boy from Coober Pedy is due to face the Youth Court today after being charged in relation to a break-in and car theft at a local caravan park l...

Drink-Driver Stopped in Coober Pedy

Far North Region – South Australia Police Just after 10 pm on Sunday 21 December 2025, officers from South Australia Police stopped a Holden station wagon on...

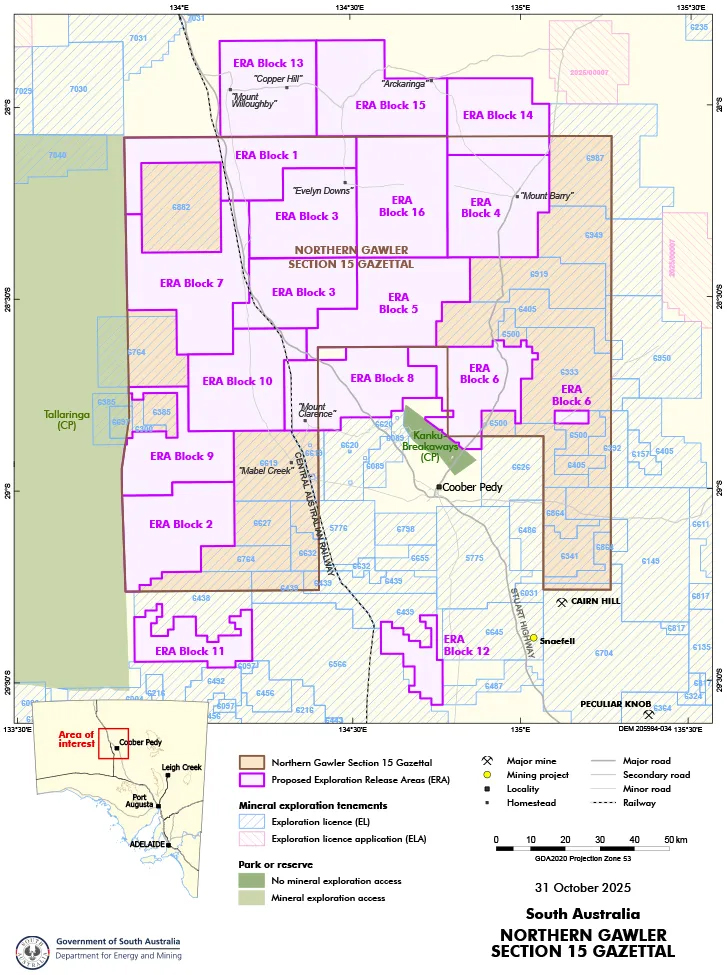

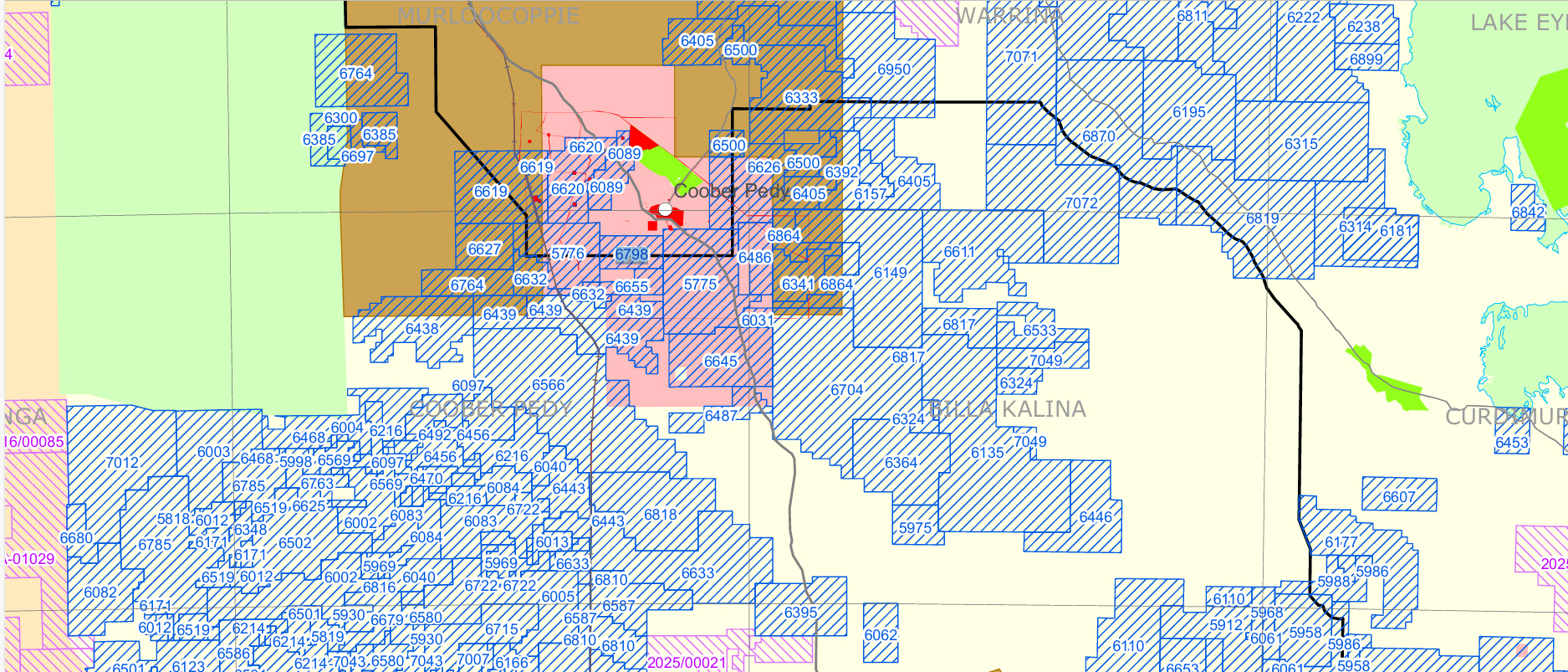

New Exploration Release Raises Fresh Fears for the Future of the Opal Industry

The South Australian Government has announced more than 11,000 km² of new Exploration Release Areas (ERAs) in the Northern Gawler Craton, opening 16 parcels ...

Knife Incidents at School Spark Questions Over Student Safety and Departmental Policy

A series of concerning reports from local students this year has raised fresh questions about the effectiveness of current school safety policies, particular...

Suspicious Blaze Destroys Vacant Coober Pedy Property Amid High Fire Danger

Police are investigating a suspicious early-morning fire that completely destroyed a vacant property in Coober Pedy on Sunday. Emergency services were called...

Are We Watching the Death of Australia’s National Gemstone in Real Time?

An Early Investigation Into the Quiet, Troubled Future of Australia’s Opal Fields Australia’s opal industry has survived droughts, depressions, and the tumbl...

High-Speed Chase Ends in Arrest Near Coober Pedy

COOBER PEDY — A man has been arrested after a high-speed police pursuit through the state’s Far North ended in scrubland north of Coober Pedy on Sunday morni...

Council Defunding of “Coober Pedy Together” a Win for Ratepayers — But Questions Remain

By The Coober Pedy News Desk November 9, 2025 The District Council of Coober Pedy has confirmed it will no longer be funding Coober Pedy Together (CPT) — a d...

Opinion: Coober Pedy Should Beware the Fine Print Behind the Promise

When Minister for Local Government Joe Szakacs stood in Parliament last week and confidently declared that “the Coober Pedy community will be out of administ...

Opinion: Six Years of Silence — What Really Happened to Coober Pedy?

By a concerned local resident (This article reflects the author’s personal opinions based on observation, rumour, and circumstance. Readers are encouraged to...

Coober Pedy Together: A Community Group or a Closed Circle?

Coober Pedy Together Incorporated, a “community group” that claims to represent the town’s vision and progress, has come under scrutiny following the release...

Two Men Banned from Driving After Separate Drink-Driving Incidents in Coober Pedy

Two men will be off the roads for a year after being caught drink-driving within minutes of each other in Coober Pedy early this morning. At 12.20am today (F...

Possible Serial Arson Threatens Coober Pedy

Late last night, Coober Pedy residents were alarmed when South Australia Police responded to a report of a suspicious fire at a property in town. Authorities...

Coober Pedy Together ride again

The renewal of the Coober Pedy Together facilitator’s $80,000-a-year contract has left many locals shaking their heads. Rate payers flooded the Minister’s of...

District Council of Coober Pedy Website Offline for Over a Week — Silence from Council Raises Alarm

Coober Pedy, South Australia — The official website of the District Council of Coober Pedy has been offline for more than a week, leaving residents, stakehol...

Disqualified drink-driver stopped in Coober Pedy; highway speeder cops $1,841 fine

COOBER PEDY, 15 September 2025 — Far North police intercepted two dangerous drivers across the region in separate incidents overnight and on Sunday afternoon...

Woman Caught Drink Driving at Coober Pedy

South Australia Police have reported a woman for drink driving after she was stopped on the Stuart Highway at Coober Pedy earlier this week. Just before midn...

Solar cars roar silently through Coober Pedy: leaders split by minutes at the checkpoint

Coober Pedy — The Bridgestone World Solar Challenge hit the opal capital this morning with a razor-thin gap between the front-runners. Brunel Solar Team (Net...

Clontarf Academies Visit Coober Pedy for Action-Packed Two Days

Coober Pedy welcomed students from five Clontarf Foundation academies this week, with boys from Port Pirie, Woodville, Murray Bridge and Christie’s Beach joi...

Variety Bash Rolls into Coober Pedy with Colour, Characters, and a Cause

This morning, Coober Pedy Area School was transformed into a carnival of colour and laughter as the Variety Bash rolled into town. The annual charity motorin...

“It’s Not a Billboard, It’s a Box with Dreams” – The Great Coober Pedy Container Conundrum

In a town built on ingenuity, grit, and the occasional well-timed “grey area,” it takes a special kind of boldness to raise eyebrows. But that’s exactly what...

Driver Killed in Tragic Crash at Pimba

A 54-year-old woman has died in a collision between a car and a road train at the intersection of the Stuart Highway and Olympic Dam Highway at Pimba on Thur...

Teens Charged After Break-In at Coober Pedy Sports Club

Coober Pedy – 2 June 2025 Two local teenagers have been charged following an alleged break-in at a sports club in Coober Pedy on Sunday afternoon. At around ...

Mystery Visitor Lands in Coober Pedy: A Lone Pelican on a Long Journey

Coober Pedy residents were treated to an unusual and magnificent sight this week—a lone pelican, hundreds of kilometres from the nearest coastline, was spott...

Drive-In Plan Rejected: Is It Time to Put This $7.5M Idea to Bed?

.newslink { color: #FF0000 !important; } .newslink:visited { color: #800000 !important; } COOBER PEDY, 27 May 2025 — The results are in, and the message from...

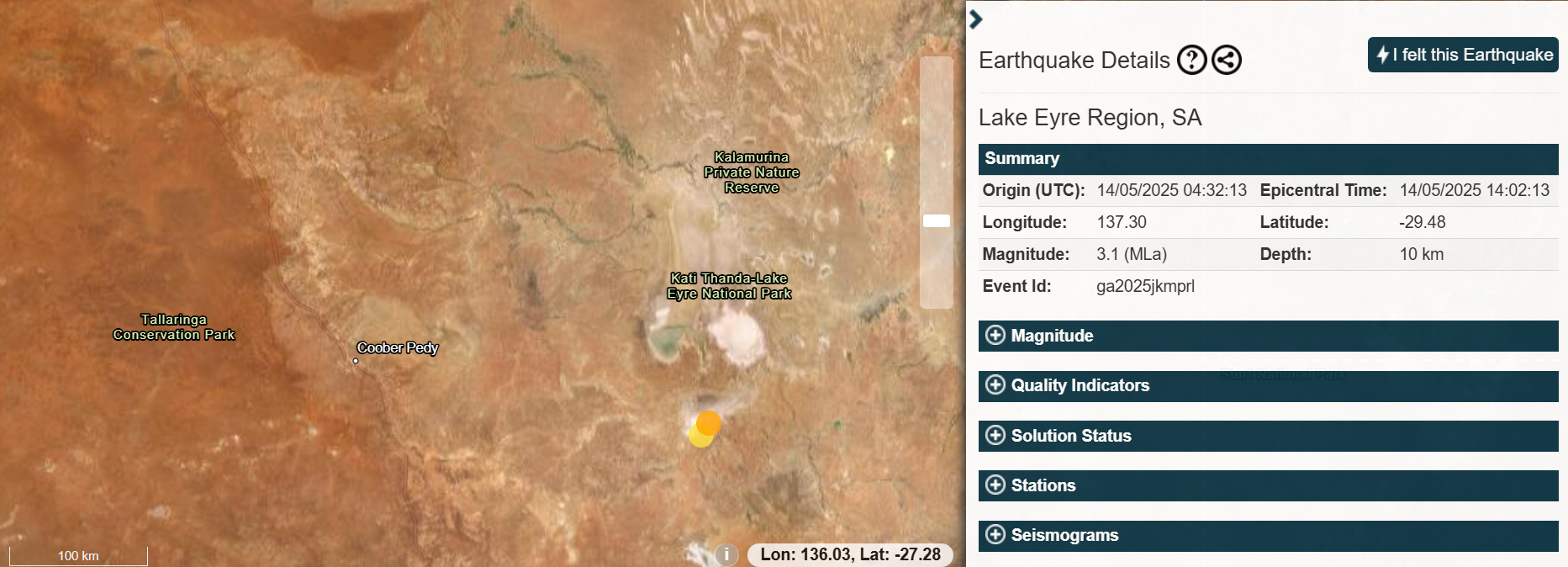

Lake Eyre is Speaking—Are We Listening?

In the past two days, two earthquakes have rattled the southern end of the Lake Eyre system—a region long considered geologically stable and far from any kno...

School Canteen Reopens to Huge Welcome at Coober Pedy Area School

The Coober Pedy Area School canteen officially reopened its doors today after being closed for several years due to COVID-19 restrictions — and it did so wit...

Coober Pedy Gears Up for a Spectacular Easter Weekend: Gems, Racing, Shooting, and Cinema Under the Stars

Coober Pedy is set to dazzle visitors this Easter long weekend (April 18–20) with a packed lineup of events showcasing the town’s vibrant outback culture. Fr...

Opinion: Stop the Fear – Coober Pedy Isn’t the Crime Capital You Think It Is

Coober Pedy – known for its opals, underground homes, and outback charm – is sadly being misrepresented by a rising tide of sensationalist storytelling and v...

Opinion: Coober Pedy’s Film Future – Hijacked, Forgotten, and Left in the Dust

Back in 2022, the District Council of Coober Pedy made a promising move: they commissioned a $30,000 feasibility study to explore the idea of a National Outb...

Suspicious Shed Fire Under Investigation in Coober Pedy

Coober Pedy, 5 April 2025 — Police are investigating a suspicious fire that destroyed a shed in Coober Pedy during the early hours of Saturday morning. Emerg...

OPINION: Coober Pedy Together – Or Just Together in Spending?

In a town struggling with the rising cost of living, dwindling health services, and ongoing education concerns, the community should be asking one very impor...

Opinion: Washington Post Got It Wrong on Coober Pedy — Here's the Truth

On January 31st, the District Council of Coober Pedy shared a post on Facebook inviting locals to speak with The Washington Post, saying the global outlet wa...

Sniffer Dog Leads to Major Cannabis Bust in Coober Pedy

Coober Pedy, SA – March 2025 Police in Coober Pedy have uncovered a significant quantity of illicit drugs thanks to the keen nose of Police Dog Neave, who sn...

Freak Electrical Storm Strikes Coober Pedy: Community Thanks Linesmen for Swift Power Restoration

Coober Pedy experienced an intense electrical storm on the afternoon of March 19, 2025, as a sudden and violent weather system swept through the area, delive...

The Disappearance of Judy

Judy, 80, was last seen at 7:30 AM on Wednesday, March 12, when she checked out of her accommodation in Coober Pedy. She was driving a white 2017 Mitsubishi ...

Coober Pedy Woman Among Three Arrested After Firearm and Drug Seizure and Driver caught speeding 60kph over limit

A Coober Pedy woman is among three people arrested after Northern District police uncovered a loaded firearm and illicit drugs in a vehicle at Munno Para Wes...

Massive Late-Night Explosion Shakes Coober Pedy January 31, 2025 – Coober Pedy, SA

A powerful explosion rocked Coober Pedy late on the night of January 30 at 11:42 PM, startling residents across the town and sparking widespread speculation ...

Stealth, Secrecy, and Environmental Risk: The Cooper Basin Carbon Storage Scandal

In an astonishing display of corporate arrogance and government complicity, Santos and Beach Energy have pushed ahead with their controversial carbon capture...

Why Did the South Australian Government Approve a Carbon Capture Exploration License in the Arckaringa Basin Despite Federal Warnings?

In a move that raises serious environmental and governance concerns, the South Australian Department of Energy and Mining, under Mr. Benjamin Zammit, recentl...

The Arckaringa Basin: A Treasure Worth Protecting from Carbon Capture Storage Risks

The Arckaringa Basin, nestled beneath the iconic outback town of Coober Pedy, is much more than an expanse of land. It is a vital resource that sustains the ...

Unexplained Lights Over Coober Pedy: Military Testing or Something Else?

Coober Pedy, SA – Last night, the skies to the southwest of Coober Pedy came alive with mysterious aerial displays, leaving residents and amateur skywatchers...

Mysterious UAP Sightings Spark Global and Local Curiosity

Over recent months, unidentified aerial phenomena (UAPs), commonly referred to as UFOs, have captured the world’s imagination and fuelled speculation. These ...

Opinion Piece: The Real Story Behind SA’s “Dangerous Country Crime Hotspots”

Today, South Australians were treated to a front-page fear campaign courtesy of The Advertiser. Their headline, “Exposed: SA’s Most Dangerous Country Crime H...

Driver Caught Six Times Over Legal Alcohol Limit in Port Augusta

A 48-year-old Davenport man has been arrested after being caught driving with a blood alcohol reading almost six times the legal limit. The incident occurred...

Coober Pedy: Voted One of South Australia’s Friendliest Towns by World Atlas

Coober Pedy has earned a glowing accolade as one of South Australia’s top 10 friendliest towns, according to World Atlas. This recognition celebrates the war...

Water Birds in Coober Pedy: A Sign of Big Things to Come?

Coober Pedy had several unusual visitors gracing our desert town today: water birds! A number of vibrant kingfishers were spotted across various locations, a...

Coober Pedy Police Station to See Improved Front Counter Hours

For years, Coober Pedy residents visiting the local police station during business hours often found it closed. Although the station has traditionally operat...

Council's CP30 Plan: Ambition Deferred, A Community Betrayed

The 2019 CP30 Town Plan, once hailed as a visionary roadmap for Coober Pedy's future, now stands as a stark testament to council's failure to deliver on its ...

Freak Summer Storm Brings Flash Flooding and Lightning to Coober Pedy

A freak summer storm swept through Coober Pedy today, drenching the desert town with an intense downpour and lighting up the skies with an electrical storm t...

Coober Pedy: A Town Under Siege by State-Appointed Administration

In 2019, Coober Pedy witnessed the beginning of a state-led intervention that was supposed to save the town from financial ruin. Instead, nearly six years la...

Coober Pedy Primary Graduates Celebrate Milestone at Big Winch 360

The Coober Pedy Area School hosted a graduation ceremony for its Year 6 students at the iconic Big Winch 360. These bright young students are set to embark o...

Coober Pedy Christmas Cheer: Join the Town’s festive celebrations

As the festive season approaches, the unassuming dusty town of Coober Pedy is gearing up for Christmas celebrations. Nestled in the vast expanse of South Aus...

Request for Information: Missing Vehicle

I am seeking assistance in locating my vehicle, which was loaned to a friend and is now missing. The car, a white Holden Commodore station wagon with registr...

Speedway Season Finale Thrills Crowd with 12-Year-Old Xavier's Debut Behind the Wheel

Coober Speedway bid farewell to the 2024 racing season with a night of high-octane action and unforgettable performances. Local legends Mick Farkas and Verdu...

Coober Pedy’s Drive-In Revival: A Big Screen Comeback!

Coober Pedy’s beloved drive-in movie screen, an iconic symbol of community and entertainment, is finally on its way back after a number of unexpected setback...

.JPG)

Coober Pedy Looks to Brighter Horizons Amid Tourism Challenges

Coober Pedy, South Australia’s iconic opal capital, has faced a tough tourism season this year, with numbers down by at least 30%—some suggesting as high as ...

Coober Pedy's New Digital News Service: A Voice for Locals, By Locals

Coober Pedy has unveiled an exciting new digital news platform, offering locals the chance to share their stories, report on events, and contribute to the ri...